Based on the last three years, the EVE economy should pick up in September. I have my doubts. Just as people who flee a hurricane often don't return home (think the effect Hurricane Katrina had on the population of New Orleans in 2005), I expect many players won't return to EVE due to the massive disruptions to their game play. I also think problems in the RMT portion of the economy will continue and drag down the overall economy. As for the activities that require flying around in space, I fully expect the number of NPCs killed to drop in September, leading to another drop in the bounty ISK faucet. Perhaps growth and activity rates will return somewhat to normal, but for now, I don't see the situation improving until October.

- The Nosy Gamer, "Hurricane Hilmar", 11 September 2019

The monthly economic report for September came out Friday and I am still scrambling to catch up. I published a look at the NPC and player kill data for known space on Saturday, then spent most of the rest of the weekend either looking at data or finishing up my online class. Not a lot of time for playing video games, but a lot of time considering the EVE Online economy.

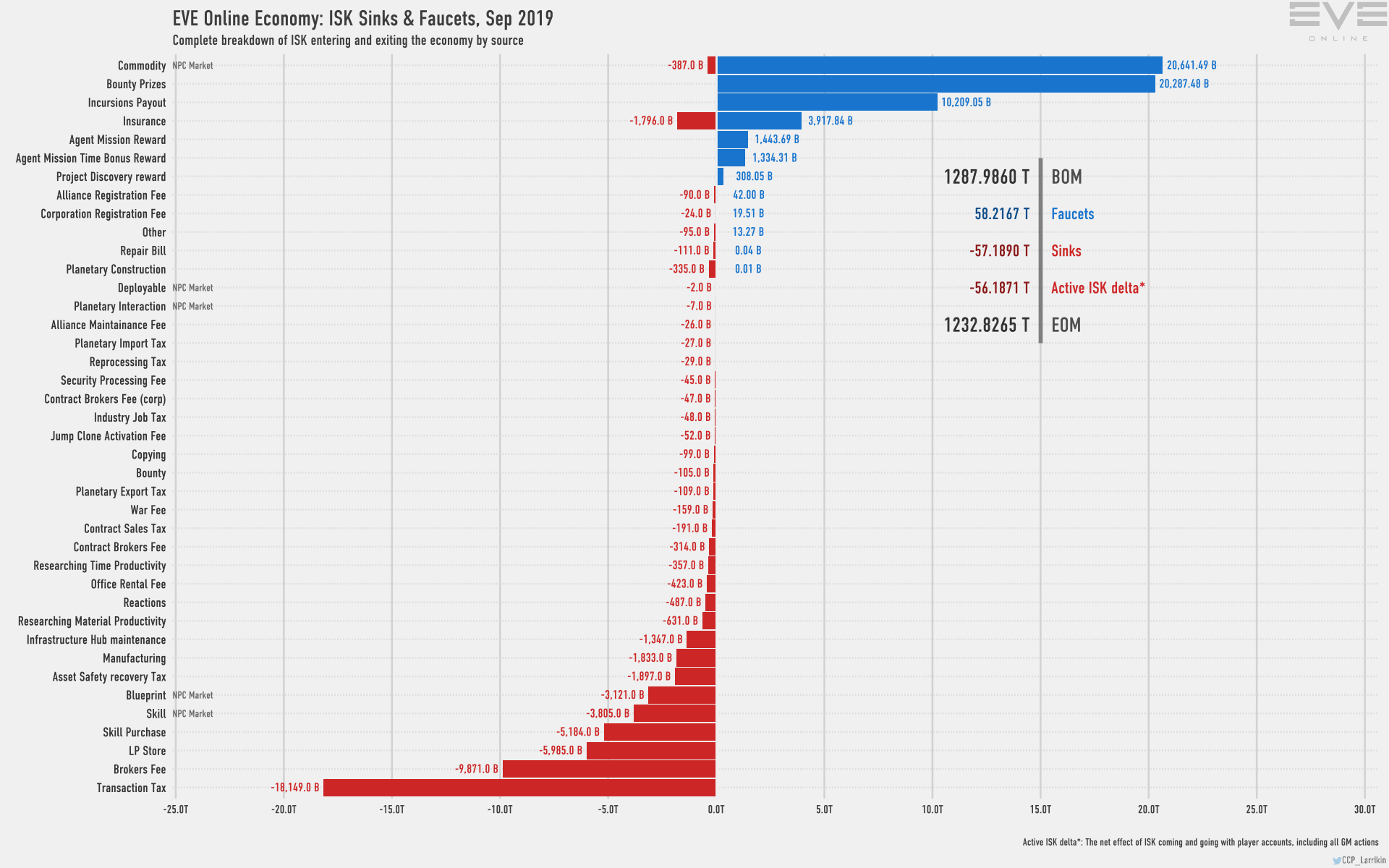

Two of CCP's goals are reducing the money supply and bringing the faucets and sinks into balance. In September, the money supply shrank another 4.3%, from 1,288 trillion ISK down to 1,232.8 trillion ISK. Going back to the end of June, the amount of ISK in the New Eden economy shrank 122.6 trillion, a 9% reduction during the so-called "Chaos Era".

Bounties, for the second month in a row, remained the second largest ISK faucet behind commodities. The gap, however, shrank to 354 billion ISK as commodity income fell nearly 3.2 trillion ISK, or 13.4% in September. Most of the decrease occurred in wormholes, as income in that area of space fell by over 2 trillion ISK. Overall, ISK faucets fell another 9% in September. Between June and September, the amount of ISK flowing into the game on a monthly basis dropped by 31.8%.

In September, currency sinks slowed down even faster than faucets. August saw an increase in taxes and fees that players apparently partially mitigated by training the Accounting and Broker Relations skills, which also received boosts two months ago. Still, the 19% reduction in taxes and broker fees collected was not all players training up their market skills. Overall, ISK faucets removed 18.3% less ISK in September than the month before. Going back to the beginning of summer, players payed 10% less in taxes and fees in

Looking at the summary data Friday was an "Oh, shit!" moment. In a month that historically sees relative stability (an average -0.2% decline from 2016-2018), the New Eden economy contracted by 12.6% in September 2019. All the racket readers may hear in the background are talking heads moving goalposts.

With Hurricane Hilmar (the institution of delayed, wormhole-style local in null security space) over on 16 September, the time came to look at the damage to the economy. From June to September, the economy had shrunk by 24.9%. The average during the summers of 2016-2018 was a decline of 10.3%. A decline so large I started wondering about the worst economic quarters in EVE history.

The third quarter of 2019, a period dominated by Hurricane Hilmar, was the sixth quarter going back to 2004 which experienced an economic contraction greater than 10%. Of the six quarters, four had experienced a quarter with over 50% growth immediately preceding the decline. The top three declines in quarterly economic activity were all related to Upwell structures.

The quarter with the largest contraction, Q1 2019, immediately followed the Onslaught expansion in November 2018 that introduced three new Upwell structures: the Ansiblex Jump Gate, Pharolux Cyno Beacon, and Tenebrex Cyno Jammer. The resulting massive infrastructure spending by the major null sec alliances in Q4 2018 resulted in a massive decline in economic activity in the first three months of 2019. The next largest decline, 36.7% in Q1 2018, followed the Lifeblood expansion released at the end of October 2017. The fourth quarter of 2017 witnessed the introduction of active moon mining, with refineries required for fracking operations to extract moon minerals. Once again, a massive infrastructure operation saw a decline in the economy after the frenetic activity to replace corp and alliance level income ended. The final Upwell-related decline occurred in Q4 2016. The Citadel expansion in April 2016 introduced Astrahus, Fortizar, and Keepstar Upwell structures to the game, and players began a massive effort to replace their existing POS.

The fifth largest quarterly contraction, the second quarter of 2016, was also a response to new content added to EVE in the previous quarter. In Februrary 2016, CCP not only introduced the skill trading system, but also seeded the Force Auxiliary skills for all races as well as the skill books for Light & Support Fighter skills.

The last quarter with a double-digit contraction in economic activity, Q4 2009, is somewhat of a mystery. Not only was the quarter the only one on the list that followed a quarter that also had an economic decline, but the quarter was part of EVE Online's first recession. The closest I can come to an explanation is the length of time between the two expansions in 2009. The first, Apocrypha, introduced wormholes to the game on 10 March 2009. The second, Dominion, replaced the old POS-based sovereignty system in null sec on 1 December. Perhaps, with the release of the news of the system change on 9 September, the null sec powers of the time delayed their fighting until the new sov system was in place.

Returning to the present day, what influenced the 15.5% contraction in the quarter just passed? The recent Invasion expansion launched on 28 May only resulted in a 1.1% increase in the economy in the second quarter. Indeed, if all RMT tokens (Daily Alpha Injectors, Large Skill Injectors, Multiple Pilot Training Certificates, Pilot's Body Resculpt Certificates, Skill Extractors, and Small Skill Injectors) are removed from consideration, the economy in the second quarter actually contracted by 1%. The simplest explanation is the content in the form of Hurricane Hilmar drove the lower economic activity.

What is going to happen in October? I doubt we will see growth matching the average of the three years, if only because The Crimson Harvest had such an outsized impact in 2018. A 2% expansion in October would prove a good outcome. My only concern about such a move is the weakness in the market for the RMT tokens. If The Crimson Harvest event comes back in the next week, the numbers would go much higher. In other words, I honestly don't know. CCP currently is doing its best to keep players in the dark about what to expect in the future. This month, reading the economic data does not help shed light.

No comments:

Post a Comment